---

title: "Beyond Normality"

share:

permalink: "https://book.martinez.fyi/beyond_normality.html"

description: "Business Data Science: What Does it Mean to Be Data-Driven?"

linkedin: true

email: true

mastodon: true

---

In the preceding chapters, we basked in the warm glow of normality, a

simplifying assumption that allowed us to model outcomes as if they arose from

the familiar bell curve. Yet, the real world often serves up data generated by

far more diverse processes. Outcomes might be binary choices (to adopt or

reject), rankings on an ordinal scale (like satisfaction surveys), or simple

counts (such as the number of subscribers). In this chapter, we embark on an

expedition beyond the comfortable confines of normality, charting the terrain of

these alternative data types and the specialized tools we need to analyze them.

## Binary Outcomes: The Coin Flips of Data

Binary outcomes are the coin flips of the data world – two sides, two

possibilities. Think success/failure, yes/no, or the ever-important adopt/reject

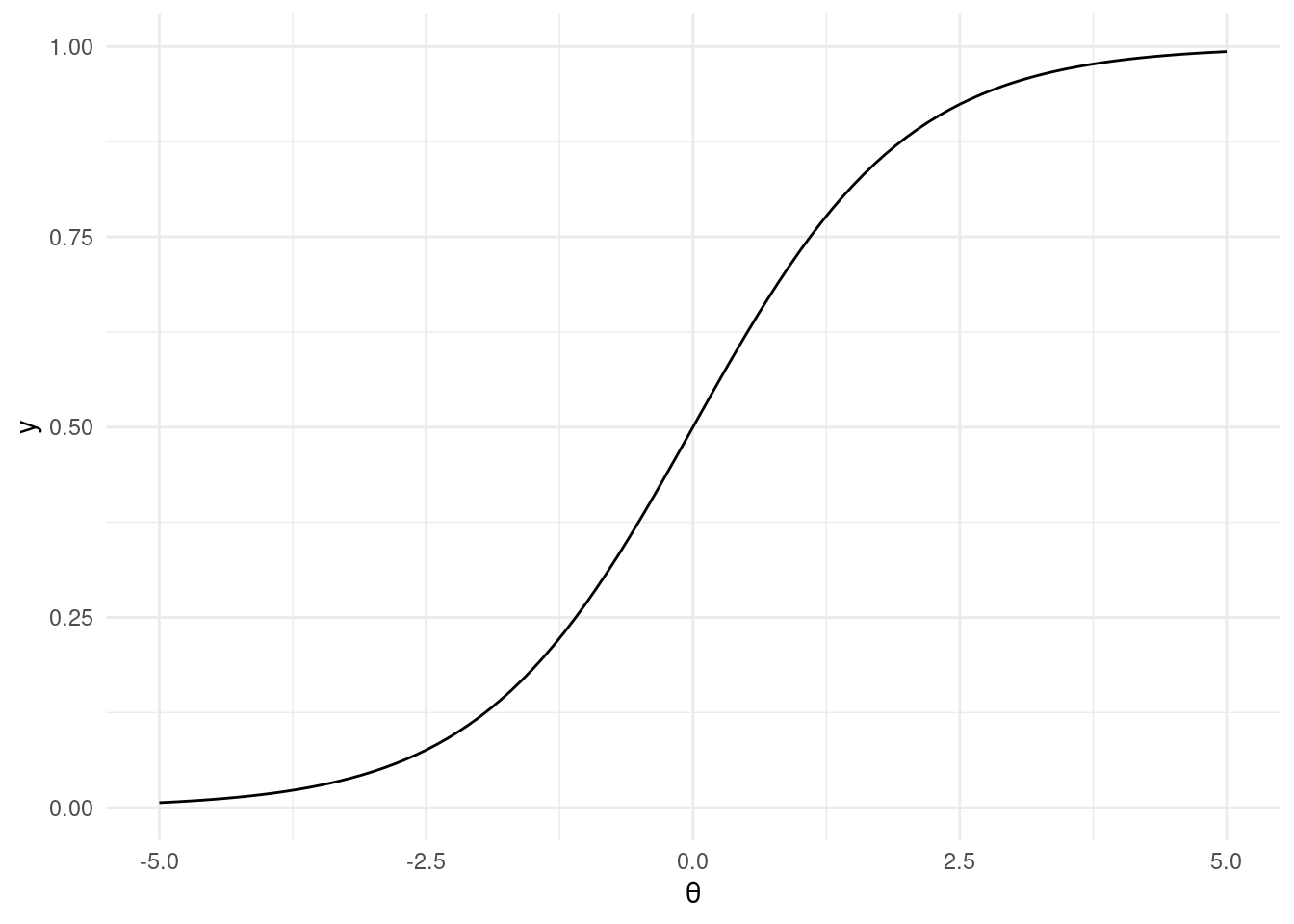

decision. To model these, we turn to the trusty logistic regression. While

linear probability models are also used, logistic regression has the distinct

advantage of keeping our predictions bounded between the sensible limits of 0

and 1.

This workhorse of a model is a type of generalized linear model, employing a

logit link function:

$$

\text{BernoulliLogit}(y|\theta) = \text{Bernoulli}(y|\text{logit}^{-1}(\theta))

$$

where

$$

\text{logit}^{-1}(\theta) = \frac{1}{1 + \exp(-\theta)}

$$

```{r inverse_logit, fig.align = 'center', message=FALSE, warning=FALSE}

library(ggplot2)

library(tibble)

library(dplyr)

inv_logit <- function(theta) {

return(1 / (1 + exp(-theta)))

}

ggplot2::ggplot() +

ggplot2::stat_function(fun = inv_logit) +

ggplot2::theme_minimal() +

ggplot2::xlim(-5, 5) +

ggplot2::xlab(expression(theta))

```

To illustrate, let's cook up some fake data:

```{r fake_data}

# Fake data

N <- 2000

K <- 2

set.seed(1982)

fake_data <- tibble::tibble(

x1 = rnorm(N, mean = 0, sd = 1),

x2 = rnorm(N, mean = 0, sd = 1),

treat = sample(

x = c(TRUE, FALSE), size = N, replace = TRUE,

prob = c(0.5, 0.5)

),

r = runif(n = N, min = 0, max = 1)

) %>%

dplyr::mutate(

p0 = inv_logit(theta = -3 + 0.1 * x1 + 0.25 * x2),

p1 = inv_logit(theta = -3 + 0.1 * x1 + 0.25 * x2 + 0.2),

y0 = dplyr::case_when(p0 > r ~ 1, TRUE ~ 0),

y1 = dplyr::case_when(p1 > r ~ 1, TRUE ~ 0),

y = dplyr::case_when(

treat ~ as.logical(y1),

TRUE ~ as.logical(y0)

)

)

dplyr::glimpse(fake_data)

mean_y0 <- mean(fake_data$y0)

mean_y1 <- mean(fake_data$y1)

impact <- round((mean(fake_data$y1) - mean(fake_data$y0)) * 100, 2)

```

In this fabricated dataset, we've engineered a scenario where, without

intervention, only `r scales::percent(mean_y0)` would have adopted the feature.

Yet, with the intervention applied universally, adoption would have jumped to

`r scales::percent(mean_y1)`. The true impact of this intervention is a hefty

`r impact` percentage points.

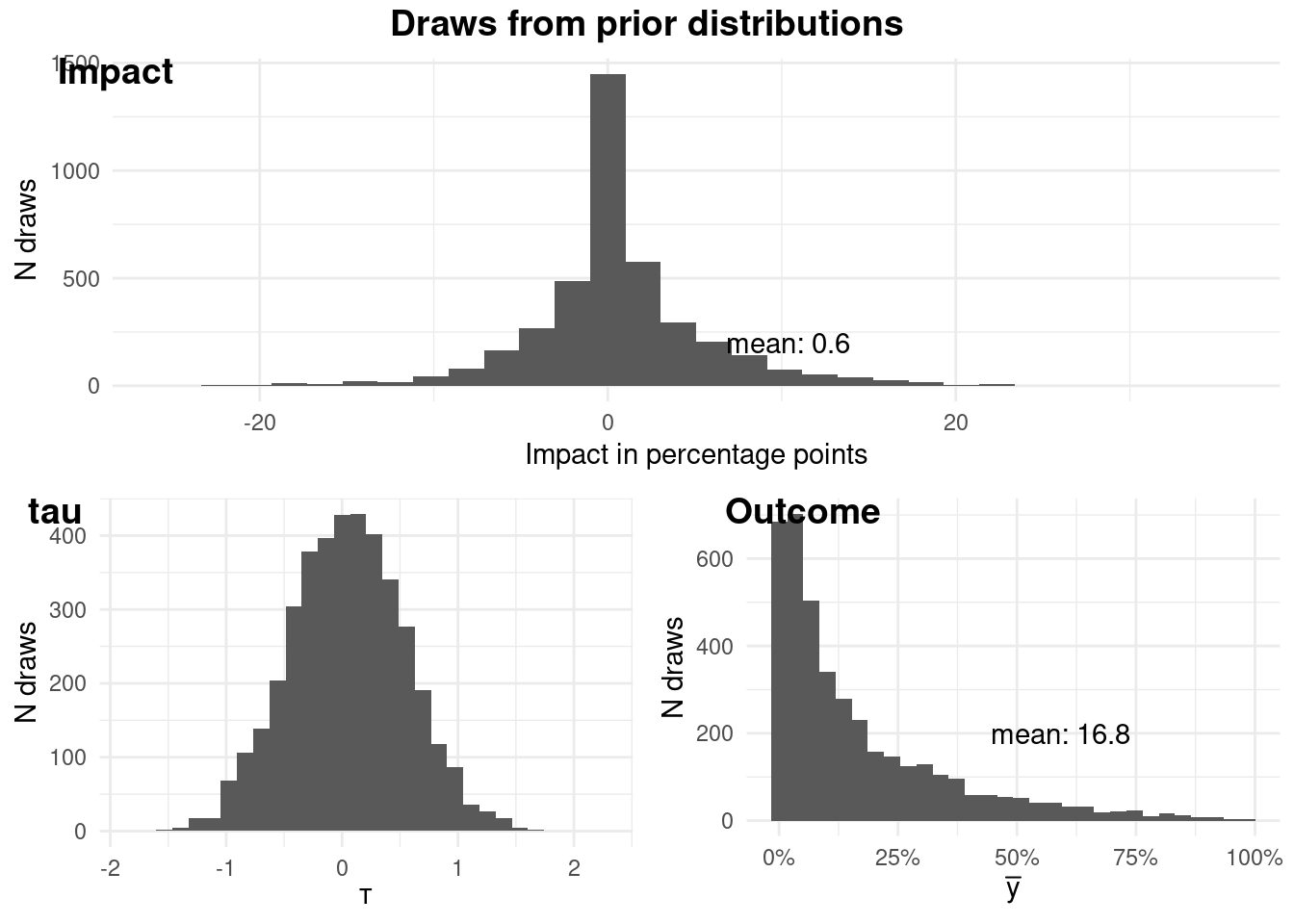

### Prior predictive checking

As Bayesians, we're not just number crunchers; we're storytellers. We weave

narratives about data, and our priors are the opening chapters. So, before we

unleash our model, let's ponder what our priors imply.

Our model takes this form:

$$

\begin{aligned}

\theta &= \alpha + X \beta + \tau T \\

\alpha &\sim N(\mu_{\alpha}, sd_{\alpha}) \\

\beta_j &\sim N(\mu_{\beta_j}, sd_{\beta_j}) \\

\tau &\sim N(\mu_{\tau}, sd_{\tau})

\end{aligned}

$$

```{r priors_check, fig.align = 'center', message=FALSE, results = "hide"}

logit <- imt::logit$new(

data = fake_data,

y = "y", # this will not be used

treatment = "treat",

x = c("x1", "x2"),

mean_alpha = -3,

sd_alpha = 2,

mean_beta = c(0, 0),

sd_beta = c(1, 1),

tau_mean = 0.05,

tau_sd = 0.5,

fit = FALSE # we will not be fitting the model

)

logit$plotPrior()

```

### Fitting the Model: Where Theory Meets Data

Satisfied with our priors, we're ready to fit the model to the data:

```{r fit, fig.align = 'center', message=FALSE, results = "hide"}

logit <- imt::logit$new(

data = fake_data,

y = "y",

treatment = "treat",

x = c("x1", "x2"),

mean_alpha = -3,

sd_alpha = 2,

mean_beta = c(0, 0),

sd_beta = c(1, 1),

tau_mean = 0.05,

tau_sd = 0.5,

fit = TRUE

)

```

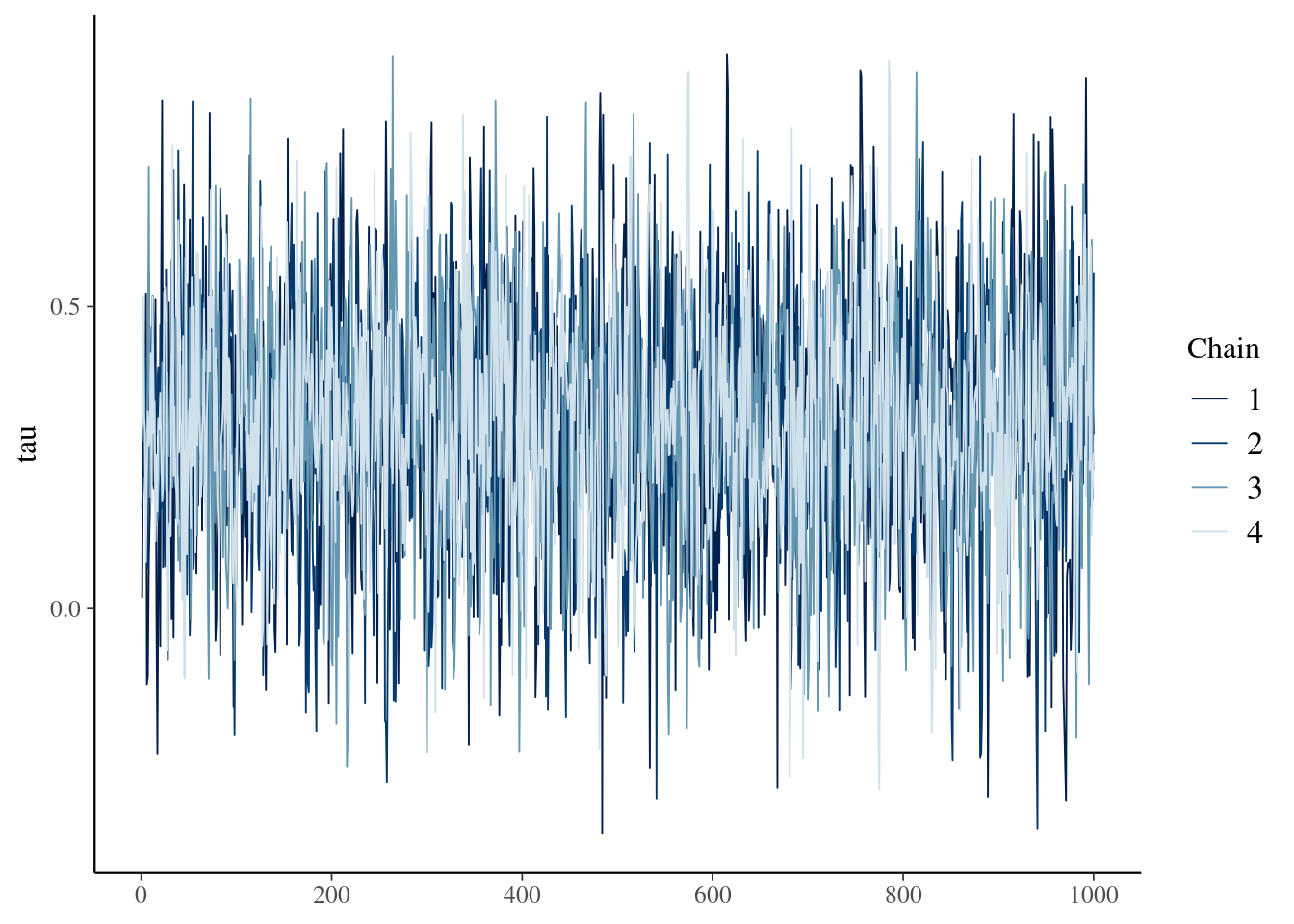

Let's glance at the trace plot of tau to ensure our chains mixed well and converged:

```{r tracePlot, fig.align = 'center'}

logit$tracePlot()

```

To sum up our findings, we have a few handy methods at our disposal:

```{r findings, fig.align = 'center'}

logit$pointEstimate()

logit$credibleInterval(width = 0.95)

logit$calcProb(a = 0)

```

We can also use the prediction function to predict new data and compare the

differences between groups. The `predict` function takes the `new_data` and

`name` argument to name the group. For example, here we will predict the data as

if all units are treated, then make another prediction as if all units are not

treated and summarize the two groups.

```{r predSummary}

fake_treated_data <- fake_data %>% mutate(treat = TRUE)

fake_control_data <- fake_data %>% mutate(treat = FALSE)

logit$predict(

new_data = fake_treated_data,

name = "y1"

)

logit$predict(

new_data = fake_control_data,

name = "y0"

)

logit$predSummary(name = "y1", width = 0.95, a = 0)

logit$predSummary(name = "y0", width = 0.95, a = 0)

```

We can also compare the differences between two groups of predictions.

```{r predCompare}

logit$predCompare(name1 = "y1", name2 = "y0", width = 0.95, a = 0)

```

We can also summarize and compare the predictions conditioning on subgroups.

```{r subgroup}

logit$predSummary(

name = "y1",

subgroup = (fake_data$x1 > 0),

width = 0.95, a = 0

)

logit$predCompare(

name1 = "y1",

name2 = "y0",

subgroup1 = (fake_treated_data$x1 > 0),

subgroup2 = (fake_control_data$x1 > 0),

width = 0.95, a = 0

)

```

Finally, we can get the posterior predictive draws for advanced analysis.

```{r getPred}

pred <- logit$getPred(name = "y1")

```

## Ordinal Outcomes

Ordinal outcomes are a rather curious beast in the realm of causal inference.

They have a natural order - think of a survey respondent rating their

satisfaction on a scale from "very dissatisfied" to "very satisfied" - but the

intervals between the values don't necessarily hold equal weight. The distance

between "dissatisfied" and "neutral" may not be the same as that between

"satisfied" and "very satisfied." This lack of equal spacing is a challenge we

must address head-on when analyzing the impact of an intervention or treatment.

This nuance of ordinal outcomes is also present in other domains, such as user

experience ratings (e.g., poor, fair, good, excellent), or educational

attainment levels (e.g., less than high school, high school diploma, some

college, college degree). In each case, there's a clear order, but the spacing

between levels is not uniform.

This lack of uniform spacing can complicate our analysis, particularly when

applying traditional regression models designed for continuous outcomes. We need

a tailored approach that respects the ordinal nature of the data, while still

allowing us to draw meaningful causal inferences.

TODO

## Count Outcomes {#sec-negative-binomial}

In this section, we're talking about events we can tally—website visits,

customer complaints, product sales, you name it. These outcomes are inherently

non-negative integers, reflecting the discrete nature of the events we're

counting.

The go-to tool for analyzing count outcomes is often Poisson regression.

However, real-world data frequently throws us a curveball in the form of

overdispersion, where the variance of the count data outstrips its mean. This is

where negative binomial regression swoops in to save the day. It's a souped-up

version of Poisson regression that accounts for overdispersion by adding an

extra parameter to the model.

Count data pops up in all sorts of scenarios. We might be interested in the

effect of a new marketing campaign on app downloads or the impact of a software

update on user logins. With count outcomes, the possibilities are as endless as

the events we can count.

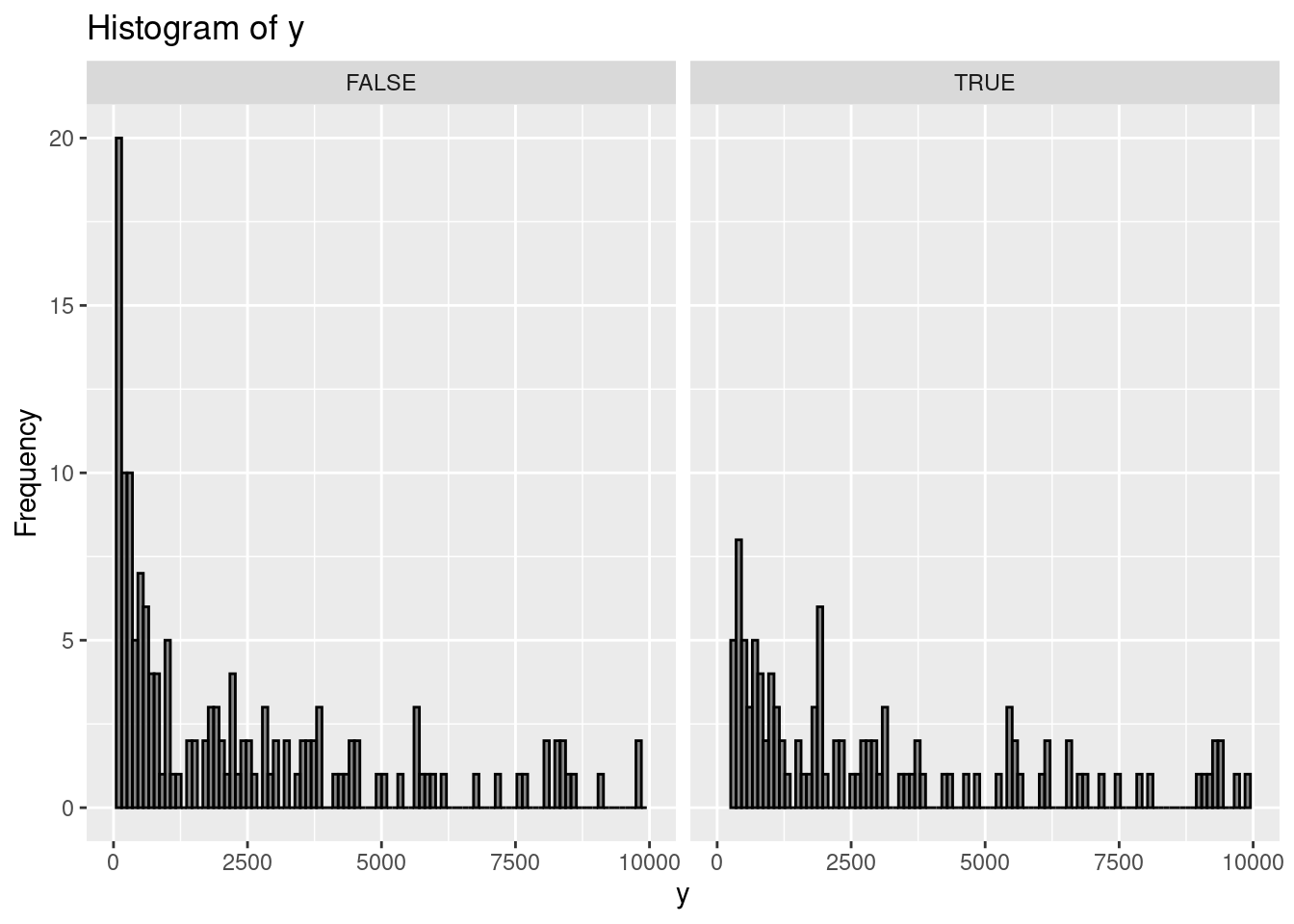

### An Example with Fake Data: Video Views Galore

Let's say we're interested in the number of views a video receives in a given

period. This is a perfect opportunity to use the negative binomial distribution

to model the underlying data-generating process. Here's how we can express this:

$$

\begin{aligned}

y_i & \sim \text{NB}(\mu_i, \phi) \\

log(\mu_i) & = \alpha + X\beta

\end{aligned}

$$

In this model, $\mu$ represents the mean (which must be positive, hence the log

link function), and the inverse of $\phi$ controls the overdispersion. A small

$\phi$ means the negative binomial distribution significantly deviates from a

Poisson distribution, while a large $\phi$ brings it closer to a Poisson. This

becomes clear when we look at the variance:

$$

Var(y_i) \sim \mu_i + \frac{\mu_i^2}{\phi}

$$

Let's whip up some fake data to illustrate:

```{r, message=FALSE, warning=FALSE}

set.seed(9782)

library(dplyr)

library(ggplot2)

N <- 1000

fake_data <-

tibble::tibble(x1 = runif(N, 2, 9), x2 = rnorm(N, 0, 1)) %>%

dplyr::mutate(

mu = exp(0.5 + 1.7 * x1 + 4.2 * x2),

y0 = rnbinom(N, size = 2, mu = mu), # here size is phi

y1 = y0 * 1.05,

t = sample(c(TRUE, FALSE), size = n(), replace = TRUE, prob = c(0.5, 0.5)),

y = case_when(t ~ as.integer(y1),

.default = as.integer(y0)

)

) %>%

filter(y > 0)

# Plotting the histogram using ggplot2

ggplot(fake_data, aes(x = y)) +

geom_histogram(

bins = 100,

color = "black",

alpha = 0.7

) +

facet_wrap(~t) +

labs(title = "Histogram of y", x = "y", y = "Frequency") +

xlim(0, 1e4) +

ylim(0, 20)

```

### OLS: A Common, But Flawed, Approach

A typical way to estimate the lift of an intervention in this scenario is to run

ordinary least squares (OLS) on the natural logarithm of the outcome. Then,

folks often look at the point estimate and 95% confidence interval for the

treatment effect. Doing this with our fake data might lead you to conclude that

the intervention is ineffective, as the 95% confidence interval includes zero.

```{r}

lm(data = fake_data, log(y) ~ x1 + x2 + t) %>% broom::tidy(conf.int = TRUE)

```

### Taming Overdispersion: The Bayesian Negative Binomial Advantage

Enter the Bayesian negative binomial model, easily implemented using the {imt}

package in R. This approach has two key advantages. First, it better captures

the true data-generating process. Second, being Bayesian, it lets us incorporate

prior information and express our findings in a way that's more directly

relevant to business decisions.

```{r NB, message=FALSE, results = "hide"}

library(imt)

nb <- negativeBinomial$new(

data = fake_data, y = "y", x = c("x1", "x2"),

treatment = "t", tau_mean = 0.0, tau_sd = 0.025

)

```

A quick check of the trace plot is always a good idea:

```{r tp}

nb$tracePlot()

```

Now for the payoff. We can readily obtain a point estimate for the impact using

`nb$pointEstimate()` (`r scales::percent(nb$pointEstimate())`) and a 95%

credible interval using `nb$credibleInterval(width = 0.95, round = 2)`

(`r nb$credibleInterval(width

= 0.95, round = 2)`). But what if we want to know

the probability that the impact is at least 1% (or any other threshold)? Easy

peasy! We use `nb$posteriorProb(threshold = 0.01)`

(`r nb$posteriorProb(threshold = 0.01)`). Finally, to visualize the evolution of

our understanding from prior to posterior, we employ `nb$vizdraws()`.

::: {.content-visible when-format="html"}

```{r vz, message=FALSE}

#| eval: !expr knitr::is_html_output()

nb$vizdraws(display_mode_name = TRUE, breaks = 0.01,

break_names = c("< 0.01", "> 0.01"))

```

:::