---

title: "Study Design"

share:

permalink: "https://book.martinez.fyi/strength.html"

description: "Pilot Strength: Designing Decision-Centric Business Experiments"

linkedin: true

email: true

mastodon: true

---

As we discussed before, the most important thing when designing a study is to

start with the decision you are trying to inform, and craft the right business

questions that can be answered with data to inform that decision. Then, if you

are going to run an experiment to answer those questions you will have to think

about important details such as how big of an experiment should I run, what

should be the unit of randomization, what proportion should be assigned to each

arm, etc. To answer these questions most people use power calculations.

## Power Calculations in Experimental Design

In the context of experimental design, power is the probability of detecting an

effect if it truly exists. In other words, it's the likelihood of rejecting the

null hypothesis when it is false. Power is intrinsically linked to Type II error

(false negative), which is the probability of failing to reject the null

hypothesis when it is actually false. Power is calculated as $1 - \beta$, where

$\beta$ represents the probability of a Type II error.

Power analysis involves determining the minimum sample size needed to detect an

effect of a given size or determining the effect size that can be detected with

a given sample size. A key concept in power analysis is the Minimum Detectable

Effect (MDE), which is the smallest effect size that the study is designed to

detect with a specified level of statistical power. Power can be conceptualized

as a function of the signal-to-noise ratio in an experiment. The "signal" refers

to the effect size, while the "noise" represents the variability within the

data. A stronger signal and lower noise lead to higher power.

Traditional power analysis focuses on Type I and Type II errors. However, Gelman

and Carlin (2014) argue that these are insufficient to fully capture the risks

of null hypothesis significance testing (NHST). They propose considering Type S

(sign) and Type M (magnitude) errors:

- **Type S error:** The probability that a statistically significant result

has the opposite sign of the true effect. This can lead to incorrect

conclusions about the direction of an effect.

- **Type M error:** The factor by which a statistically significant effect

might be overestimated. This can lead to exaggerated claims about the size

of an effect.

These errors are particularly relevant in studies with small samples and noisy

data, where statistically significant results may be misleading. Gelman and

Carlin recommend design analysis, which involves calculating Type S and Type M

errors to assess the potential for these errors in a study design.

### Methods for Performing Power Calculations

There are different methods for performing power calculations:

- **Analytical methods:** These methods use formulas to calculate power or

sample size based on the factors mentioned above. For example, the formula

for calculating the sample size needed for a two-sample t-test can be found

in many statistical textbooks .

- **Simulation methods:** These methods involve generating random data and

performing statistical tests repeatedly to estimate power. They are

particularly useful for complex study designs where analytical formulas may

not be available or accurate.

### A Simple Example with the Analytical Method

Suppose we are thinking about running an experiment and our outcome of interest

is binary and only 5% of the outcomes take the value 1. For example, this could

be an experiment for reducing churn. Imagine we are testing a new intervention

aimed at reducing customer churn, and we want to understand how large of an

experiment we need to reliably detect a reduction in the churn rate if the

intervention is effective. Our baseline churn rate is 5%, meaning that without

any intervention, approximately 5% of customers churn.

We want to use an analytical method to perform a power calculation.

Specifically, we want to investigate how the Minimum Detectable Effect (MDE)

changes as we increase the sample size of our experiment. The MDE, in this

context, represents the smallest reduction in the churn rate that our experiment

is designed to detect with a given level of statistical power.

The R code below uses the `calculateMdes` function to compute the MDE for

different sample sizes (N), assuming we are conducting a two-sample t-test to

compare the churn rates between a treatment and a control group. We set the

significance level (`sig_lvl`) to 0.05 and the desired power (`power`) to 0.80.

This means we want to design our experiment such that if there is a true effect

(reduction in churn), we have an 80% chance of detecting it as statistically

significant at the 5% significance level. The proportion assigned to treatment

(and control) p is set to 0.5, assuming equal allocation. The outcome is

specified as "binary", and `mean_y` is set to 0.05, representing our baseline

churn rate.

The code then iterates through a range of sample sizes, from 500 to 2000, and

calculates the MDE for each sample size. Finally, it generates a plot showing

the relationship between the sample size (N) and the MDE.

```{r}

library(ggplot2)

library(purrr)

calculateMdes <-

function(sig_lvl = 0.05,

power = 0.80,

N,

g = 1,

p = 0.5,

outcome = c("binary", "continuous"),

mean_y = NULL,

sigma_y = NULL,

R_sq_xy = 0,

rho = 0,

R_sq_WG = 0,

R_sq_BG = 0) {

# Input Validation (Moved up for earlier checks)

outcome <-

match.arg(outcome) # Ensure a valid outcome is selected

if (outcome == "continuous" & is.null(sigma_y)) {

stop("When outcome is continuous, you must specify sigma_y")

}

if (outcome == "binary" & is.null(mean_y)) {

stop("When outcome is binary, you must specify mean_y")

}

# Calculate Degrees of Freedom

df <- ifelse(g == 1, N - 2, g - 2)

# Calculate Factor for t-distribution

factor <- qt(p = 1 - sig_lvl / 2, df = df) + qt(p = power, df = df)

# Calculate sigma_lambdaRA_hat

if (g == 1) {

sigma_lambdaRA_hat <- sqrt((1 - R_sq_xy) / (N * p * (1 - p)))

} else {

cluster_size <- N / g

A <- 1 / (p * (1 - p))

B <- ((1 - rho) * (1 - R_sq_WG)) / (g * cluster_size)

C <- (rho * (1 - R_sq_BG)) / g

sigma_lambdaRA_hat <- sqrt(A * (B + C))

}

# Calculate sigma_y for binary outcome

if (outcome == "binary") {

sigma_y <- sqrt(mean_y * (1 - mean_y))

}

# Calculate MDE and MDES

MDE <- factor * sigma_lambdaRA_hat * sigma_y

MDES <- MDE / sigma_y

return(c(MDES = MDES, MDE = MDE))

}

# Vector of N values to explore (adjust as needed)

n_values <- seq(500, 2000, by = 100)

# Create a data frame with MDE values for different N

mde_data <- map_df(n_values, ~calculateMdes(N = .x,

sig_lvl = 0.05,

power = 0.80,

p = 0.5,

outcome = "binary",

mean_y = 0.05)) |>

dplyr::mutate(N = n_values)

# Create the plot

ggplot(mde_data, aes(x = N, y = MDE)) +

geom_line() +

geom_point() +

labs(

title = "Minimum Detectable Effect (MDE) vs. Sample Size (N)",

x = "Sample Size (N)",

y = "Minimum Detectable Effect (MDE)"

) +

theme_minimal()

```

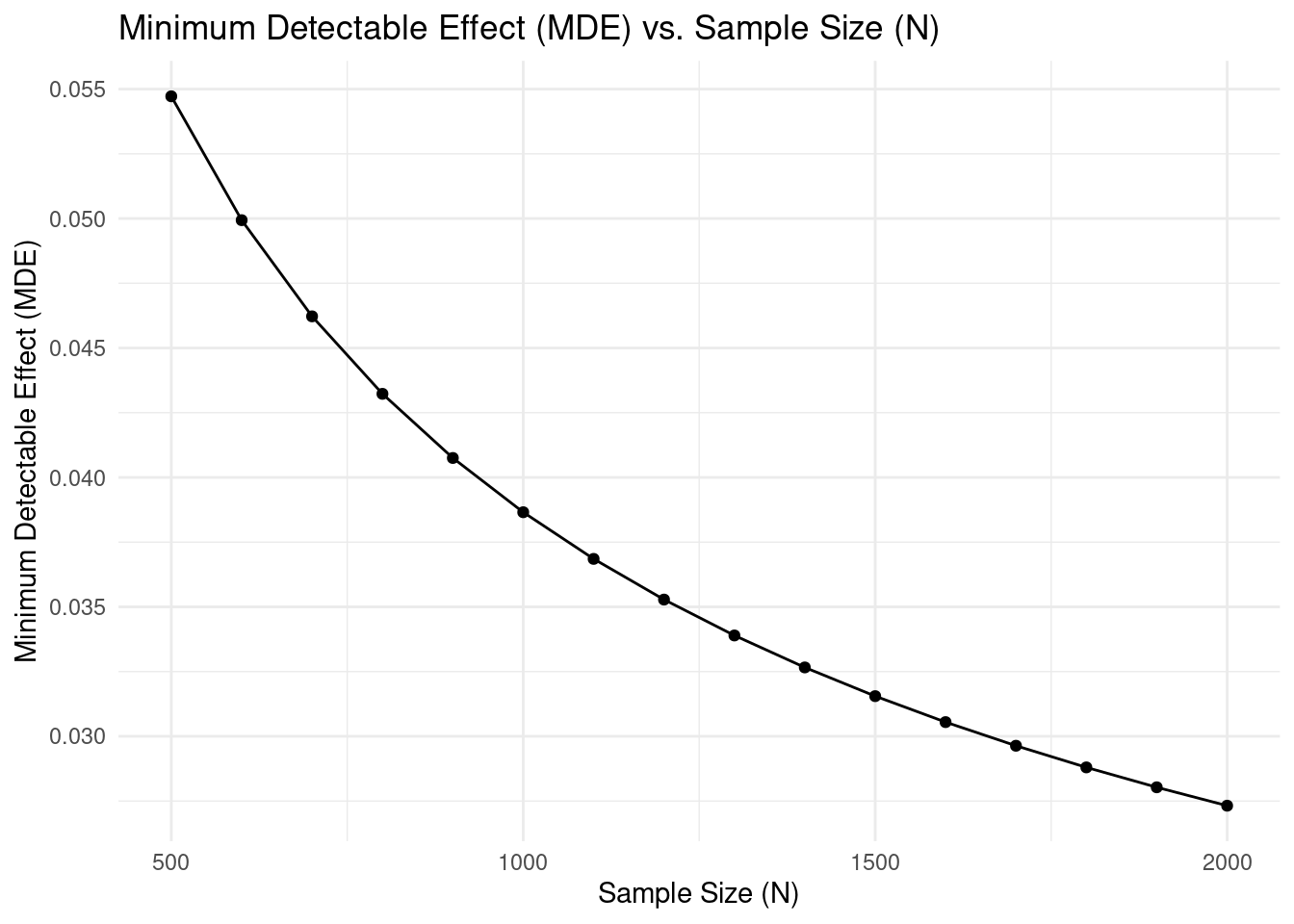

For instance, let's consider a point on the plot. If with a sample size of 1000,

the MDE is approximately

`r round(calculateMdes(N = 1000, sig_lvl = 0.05, power = 0.80, p = 0.5, outcome = "binary", mean_y = 0.05)[[2]], 2)`.

This means that with a total sample size of 1000 (500 in the treatment group

and 500 in the control group), we would be able to detect a reduction in the

churn rate of

`r round(calculateMdes(N = 1000, sig_lvl = 0.05, power = 0.80, p = 0.5, outcome = "binary", mean_y = 0.05)[[2]], 2)*100`

percentage points. If the true reduction in churn rate due to our intervention

is smaller, our experiment might not be powerful enough to detect it as

statistically significant, and we might fail to reject the null hypothesis of no

effect (even if a real, albeit smaller, effect exists).

::: callout-note

## Interpreting MDEs

The MDE curve helps you determine the tradeoff between sample size and

detectable effect size. Larger sample sizes allow you to detect smaller effects,

but at diminishing returns. When planning your study, consider both the smallest

effect size that would be practically meaningful for your business decision and

the resources required for different sample sizes.

:::

### Simulations for Type S and M Errors

To illustrate Type S (Sign) and M (Magnitude) errors in a practical context,

let's consider a simulation based on a common A/B testing scenario. Imagine a

company has a baseline customer churn rate of 5% and aims to detect an impact

of 2 percentage points through some intervention.

The simulation below assesses how frequently a study with a moderate sample size

(n=500 per group) might incorrectly estimate the direction or exaggerate the

magnitude of the observed effect:

Now lets run some simulations to estimate type S and M errors. The code below

runs 10,000 simulations with 500 observations in the treatment and 500 in the

control group, 5% probability of churn for the control group, and and impact

of 2 percentage points for treated units.

```{r}

#| warning: false

#| message: false

library(tidyverse)

library(broom)

estimateTypeSM <- function(p_true_control, lift, n_per_group, alpha, n_sim) {

p_true_variant <- p_true_control + lift

simulations <- tibble(

control_successes = rbinom(n_sim, n_per_group, p_true_control),

variant_successes = rbinom(n_sim, n_per_group, p_true_variant)

)

prop_tests <- map2_df(simulations$control_successes, simulations$variant_successes,

~ tidy(prop.test(c(.x, .y),

n = c(n_per_group, n_per_group),

correct = FALSE))) %>%

mutate(diff = estimate2 - estimate1)

significant_results <- prop_tests %>%

filter(p.value < alpha)

significant_count <- nrow(significant_results)

if(significant_count > 0) {

type_s_rate <- mean(significant_results$diff * lift < 0) * 100

exaggeration <- mean(abs(significant_results$diff) / abs(lift))

} else {

type_s_rate <- 0

exaggeration <- NA

}

list(

significant_count = significant_count,

type_s_rate = type_s_rate,

exaggeration = exaggeration

)

}

results <- estimateTypeSM(p_true_control = 0.05, lift = 0.02, n_per_group = 500, alpha = 0.05, n_sim = 10000)

```

Out of the 10,000 simulations, only `r results$significant_count` yielded a

statistically significant result. Among these statistically significant results,

`r round(results$type_s_rate, 2)`% incorrectly estimated the direction of the

effect (Type S error). The average exaggeration of the effect size (Type M

error) among the significant results was `r round(results$exaggeration, 2)`x.

## Profit-Maximizing A/B Testing: A Test & Roll Approach

Traditional power calculations in A/B testing focus on managing statistical

significance by controlling Type I and Type II errors. However, in practical

business experiments, the primary goal isn't merely to "reject the null

hypothesis" but to maximize overall profit. The test & roll framework,

introduced by @mcdonnell2018test, re-frames sample size determination as a

strategic decision balancing the cost of learning against the opportunity cost

of deploying a suboptimal treatment.

### Balancing Learning and Opportunity Cost

In conventional A/B tests, achieving high statistical power often requires large

test groups, inadvertently exposing more customers to potentially inferior

treatments. The test & roll framework explicitly addresses two crucial

considerations:

- **The cost of testing:** Every unit allocated to the test phase may

experience a less-than-optimal treatment.

- **The benefit of deployment:** Once the better treatment is identified, it

can be applied to the remainder of the population to maximize profit.

By quantifying these trade-offs explicitly, the optimal (profit-maximizing) test

size is typically smaller than traditional hypothesis testing methods recommend,

particularly when data responses are noisy or population size is limited.

### A Closed-Form Insight

@mcdonnell2018test derived a closed-form formula for determining optimal test

sizes under symmetric Normal priors (assuming no initial preference between

treatments). Formally, the optimal sample size grows as follows:

$$ n^* \propto \sqrt{N} \quad \text{and} \quad n^* \sim \mathcal{O}\left(\frac{s}{\sigma}\right) $$

This implies:

- Optimal test size ($n^*$) scales with the square root of the total available

population ($N$).

- The optimal test size is sensitive to the response noise ($s$) and the

uncertainty in treatment effects ($\sigma$).

More specifically, proposition A.2 in their paper derives:

$$

n^{*}=n_{1}^{*}=n_{2}^{*}=\sqrt{\frac{N}{4}\left(\frac{s}{\sigma}\right)^{2}+\left(\frac{3}{4}\left(\frac{s}{\sigma}\right)^{2}\right)^{2}}-\frac{3}{4}\left(\frac{s}{\sigma}\right)^{2}

$$

This contrasts with traditional power calculations, which typically recommend

sample sizes scaling linearly or super-linearly with variance, often resulting

in overly large tests.

### Extensions to Asymmetric and Complex Settings

The basic test & roll framework can also be extended to account for situations

where prior beliefs about the treatments differ. For instance:

- **Incumbent/Challenger Tests:** If one treatment is well understood (the

incumbent) and the other is more uncertain (the challenger), asymmetric

priors can be used to justify allocating a larger sample to the less-known

treatment.

- **Pricing Experiments:** When treatments involve different price points, the

trade-offs include not only response variability but also differences in

profit per sale. The framework naturally extends to these settings by

adjusting priors to reflect both the likelihood of purchase and the profit

margin.

### Operational Advantages

In practice, the test & roll design helps managers make timely decisions:

- **Smaller, Agile Tests:** By running smaller tests, firms expose fewer

customers to a potentially inferior treatment.

- **Transparency:** The decision rule is based on explicit profit

calculations, making it easier to justify the chosen test size and strategy.

- **Comparable Performance:** Despite its simplicity, the test & roll approach

has been shown to achieve regret—and thus overall performance—that is

comparable to more complex, continuously adaptive methods like Thompson

sampling.

### Summary

By centering experimentation on maximizing business impact rather than solely

achieving statistical significance, the test & roll framework presents a robust,

economically efficient alternative to traditional power-based approaches. It

optimally manages the trade-offs between learning and earning, particularly

advantageous for noisy data or limited customer populations.

## Pilot Strength: A Decision-Centric Approach

Instead of focusing solely on traditional power calculations, let's explore a

slightly different concept: pilot strength. Pilot strength represents the

probability of making the correct decision based on a pilot study with specific

characteristics and assumptions. For instance, we can examine how sample size

influences the strength of a pilot. This decision-centric approach proves

particularly valuable when the traditional frequentist framework might fail to

reject the null hypothesis, yet a decision must still be made with the available

data. To calculate pilot strength, we'll employ simulations.

### Generating Synthetic Data

Let's start by generating synthetic data. Similar to the previous example, we'll

consider a binary outcome like customer churn and an intervention that could

potentially impact it. In our synthetic data, we'll assume the new feature

increases churn by 2 percentage points. Our goal is to decide whether to roll

out this new feature, with the understanding that we should avoid the rollout if

the impact on churn exceeds 1 percentage point.

We'll generate data based on the following assumptions:

1. **Equal Treatment Allocation:** A 50% probability of assignment to the

treatment group.

2. **Churn Probabilities:** A churn probability of 5% for the control group

and 7% for the treatment group.

3. **Time Periods:** Data collection across three time periods, with 20% of

observations in period 1, 50% in period 2, and 30% in period 3.

```{r}

#| warning: false

#| message: false

library(dplyr)

library(rstan)

library(ggpubr)

library(scales)

library(furrr)

# Create a function to generate synthetic data

generate_synthetic_data <-

function(seed,

num_observations,

treatment_proportion,

control_churn_prob,

treatment_churn_prob,

period1_proportion,

period2_proportion) {

set.seed(seed)

# Calculate number of observations in each group and period directly

num_treatment <- round(num_observations * treatment_proportion)

num_control <- num_observations - num_treatment

num_period1 <- round(num_observations * period1_proportion)

num_period2 <- round(num_observations * period2_proportion)

num_period3 <- num_observations - num_period1 - num_period2

# Create data frame using explicit group and period assignments

synthetic_data <- tibble(

id = 1:num_observations,

treat = c(rep(1, num_treatment), rep(0, num_control)),

period = c(rep(1, num_period1), rep(2, num_period2), rep(3, num_period3))

) %>%

group_by(treat) %>%

mutate(# Generate binary outcome based on group-specific probabilities

y = case_when(

treat == 0 ~ rbinom(n(), 1, control_churn_prob),

TRUE ~ rbinom(n(), 1, treatment_churn_prob)

)) %>%

ungroup() # Important: Always ungroup after group_by

return(synthetic_data)

}

# Generate synthetic data

synthetic_data <- generate_synthetic_data(

seed = 123,

num_observations = 2000,

treatment_proportion = 0.5,

control_churn_prob = 0.05,

treatment_churn_prob = 0.07,

period1_proportion = 0.2,

period2_proportion = 0.5

)

glimpse(synthetic_data)

```

The `glimpse()` output provides a summary of the synthetic\_data dataframe. It

confirms that we have 2000 observations with the variables `id`, `treat`

(treatment indicator), `period`, and `y` (binary outcome representing churn).

The true impact of the new feature is a 2 percentage point increase in churn

probability. Our objective is to estimate the probability that this impact

exceeds 1 percentage point, which would lead us to decide against rolling out

the feature.

### A Simple Stan Model to Fit the Data

We'll implement a simple Bayesian logistic regression model to analyze these

synthetic data. This approach allows us to directly estimate the probability

that the treatment effect exceeds our decision threshold.

```{stan output.var = "logit"}

data {

int N; // Number of observations

array[N] int<lower = 0, upper = 1> y; // Outcome (binary 0 or 1)

vector[N] treat; // Treatment indicator

real mean_alpha;

real sd_alpha;

real tau_mean; // Prior mean for treatment effect

real<lower=0> tau_sd; // Prior standard deviation for treatment effect

// Flag for running estimation (0: no, 1: yes)

int<lower=0, upper=1> run_estimation;

}

parameters {

real alpha; // Intercept parameter

real tau; // treatment effect parameter

}

model {

vector[N] theta; // Linear predictor (stores calculated probabilities)

// Priors

alpha ~ normal(mean_alpha, sd_alpha);

tau ~ normal(tau_mean, tau_sd);

theta = alpha + tau * treat; // Calculate linear predictor

if (run_estimation==1) {

// Likelihood with logit link function:

y ~ bernoulli_logit(theta);

}

}

generated quantities {

vector[N] y_sim;

vector[N] y0;

vector[N] y1;

real eta;

real mean_y_sim;

for (i in 1:N) {

y_sim[i] = bernoulli_logit_rng(alpha + tau * treat[i]);

y0[i] = bernoulli_logit_rng(alpha);

y1[i] = bernoulli_logit_rng(alpha + tau);

}

eta = mean(y1) - mean(y0);

mean_y_sim = mean(y_sim);

}

```

This model allows us to calculate the probability that the intervention elevates

the likelihood of churn by more than our minimum threshold. Let's create a

function to analyze our synthetic data:

```{r}

analyze_synthetic_data <-

function(data,

mean_alpha,

sd_alpha,

tau_mean,

tau_sd,

run_estimation,

periods,

threshold) {

# Filter data

if (!is.null(periods)) {

data <- data %>% filter(period %in% periods)

}

# Prepare data for Stan

stan_data <- list(

N = nrow(data),

y = data$y,

treat = data$treat,

mean_alpha = mean_alpha,

sd_alpha = sd_alpha,

tau_mean = tau_mean,

tau_sd = tau_sd,

run_estimation = run_estimation

)

# Fit Stan model

posterior <- sampling(logit, # Use the loaded stan model

data = stan_data,

refresh = 0)

if (run_estimation == 0) {

# Prior predictive check

prior_draws <- posterior::as_draws_df(posterior)

prior_eta <- prior_draws$eta

prior_tau <- prior_draws$tau

prior_mean_y <- prior_draws$mean_y_sim

# --- Create plots (using your provided structure) ---

mean_y_plot <- ggplot2::ggplot(

data = tibble::tibble(draws = prior_mean_y),

ggplot2::aes(x = draws)

) +

ggplot2::geom_histogram(bins = 30) +

ggplot2::scale_x_continuous(labels = scales::percent) +

ggplot2::annotate("text",

x = quantile(prior_mean_y, prob = 0.9),

y = 200, label = paste0(

"mean: ",

round(mean(prior_mean_y) * 100, 1)

),

hjust = 0

) +

ggplot2::xlab(expression(bar(y))) + # Using expression for y bar

ggplot2::ylab("N draws") +

ggplot2::theme_minimal()

tau_plot <- ggplot2::ggplot(

data = tibble::tibble(draws = prior_tau),

ggplot2::aes(x = draws)

) +

ggplot2::geom_histogram(bins = 30) +

ggplot2::xlab(expression(tau)) + # Using expression for tau

ggplot2::ylab("N draws") +

ggplot2::theme_minimal()

eta_plot <- ggplot2::ggplot(

data = tibble::tibble(draws = prior_eta * 100),

ggplot2::aes(x = draws)

) +

ggplot2::geom_histogram(bins = 30) +

ggplot2::annotate("text",

x = quantile(prior_eta * 100, prob = 0.9),

y = 200, label = paste0(

"mean: ",

round(mean(prior_eta) * 100, 1)

),

hjust = 0

) +

ggplot2::geom_vline(xintercept = 2,

color = "red",

linetype = "dashed") +

ggplot2::annotate(

"text",

x = 2.5,

y = 250,

label = "True Effect",

color = "red",

hjust = 0

) +

ggplot2::xlab("Impact in percentage points") +

ggplot2::ylab("N draws") +

ggplot2::theme_minimal()

# --- Combine plots with ggarrange ---

plots <- ggpubr::ggarrange(eta_plot,

ggpubr::ggarrange(tau_plot, mean_y_plot,

labels = c("tau", "Outcome"),

ncol = 2),

labels = "Impact", nrow = 2

)

plots <- annotate_figure(plots,

top = text_grob(

"Draws from prior distributions",

face = "bold",

size = 14

))

# Calculate probability above threshold

prob_above_threshold <- mean(prior_eta > threshold)

# Return the combined plot and probability

return(list(plot = plots, prob_above_threshold = prob_above_threshold))

} else {

# --- Posterior analysis (remains the same) ---

posterior_draws <- posterior::as_draws_df(posterior)

posterior_eta <- posterior_draws$eta

eta_plot <-

ggplot(data = tibble(draws = posterior_eta * 100), aes(x = draws)) +

geom_histogram(bins = 30) +

annotate(

"text",

x = quantile(posterior_eta * 100, prob = 0.9),

y = 200,

label = paste0("mean: ", round(mean(posterior_eta) * 100, 1)),

hjust = 0

) +

geom_vline(xintercept = 2,

color = "red",

linetype = "dashed") +

annotate(

"text",

x = 2.5,

y = 250,

label = "True Effect",

color = "red",

hjust = 0

) +

labs(x = "Impact (percentage points)", y = "N draws") +

theme_minimal()

prob_above_threshold <- mean(posterior_eta > threshold)

return(list(plot = eta_plot, prob_above_threshold = prob_above_threshold))

}

}

```

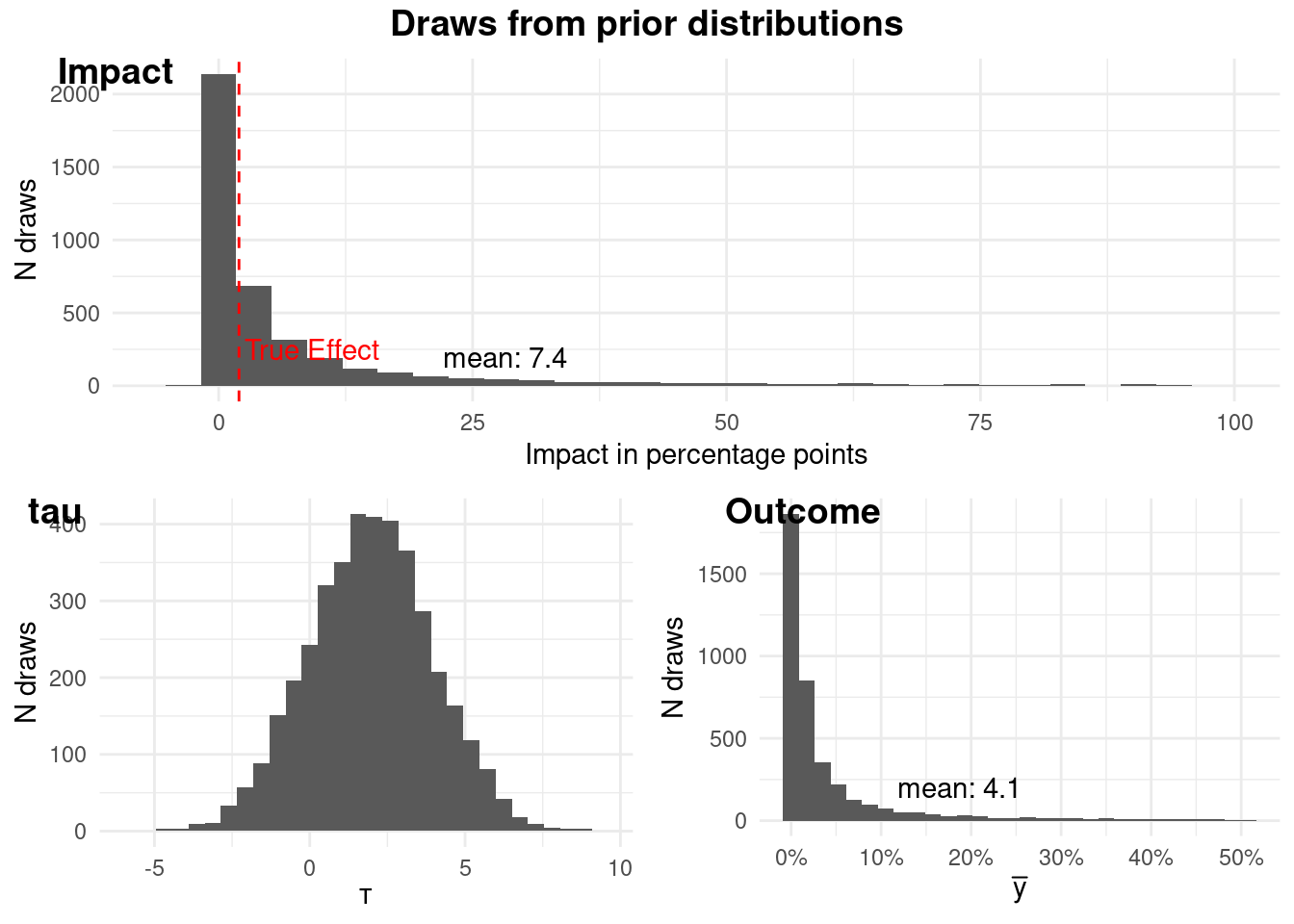

### Prior Predictive Checks

In Bayesian modeling, it's crucial to check if our prior distributions are

reasonable. We use prior predictive checks to simulate data from our prior

distributions and visually assess if these simulated datasets are plausible in

the context of our problem. If the prior predictive distributions generate

implausible data, it might indicate that our priors are misspecified.

```{r}

#| warning: false

#| message: false

prior <- analyze_synthetic_data(

data = synthetic_data,

mean_alpha = -6,

sd_alpha = 1,

tau_mean = 2,

tau_sd = 2,

run_estimation = 0,

periods = c(1, 2, 3),

threshold = 0.01

)

# Print the plot

prior$plot

```

The plots above show that our prior distributions for the outcome (churn) and

the impact of the intervention are reasonable. In particular our prior before

seeing the outcome data is that the probability that the intervention has a

meaningful impact is `r scales::percent(prior$prob_above_threshold)`.

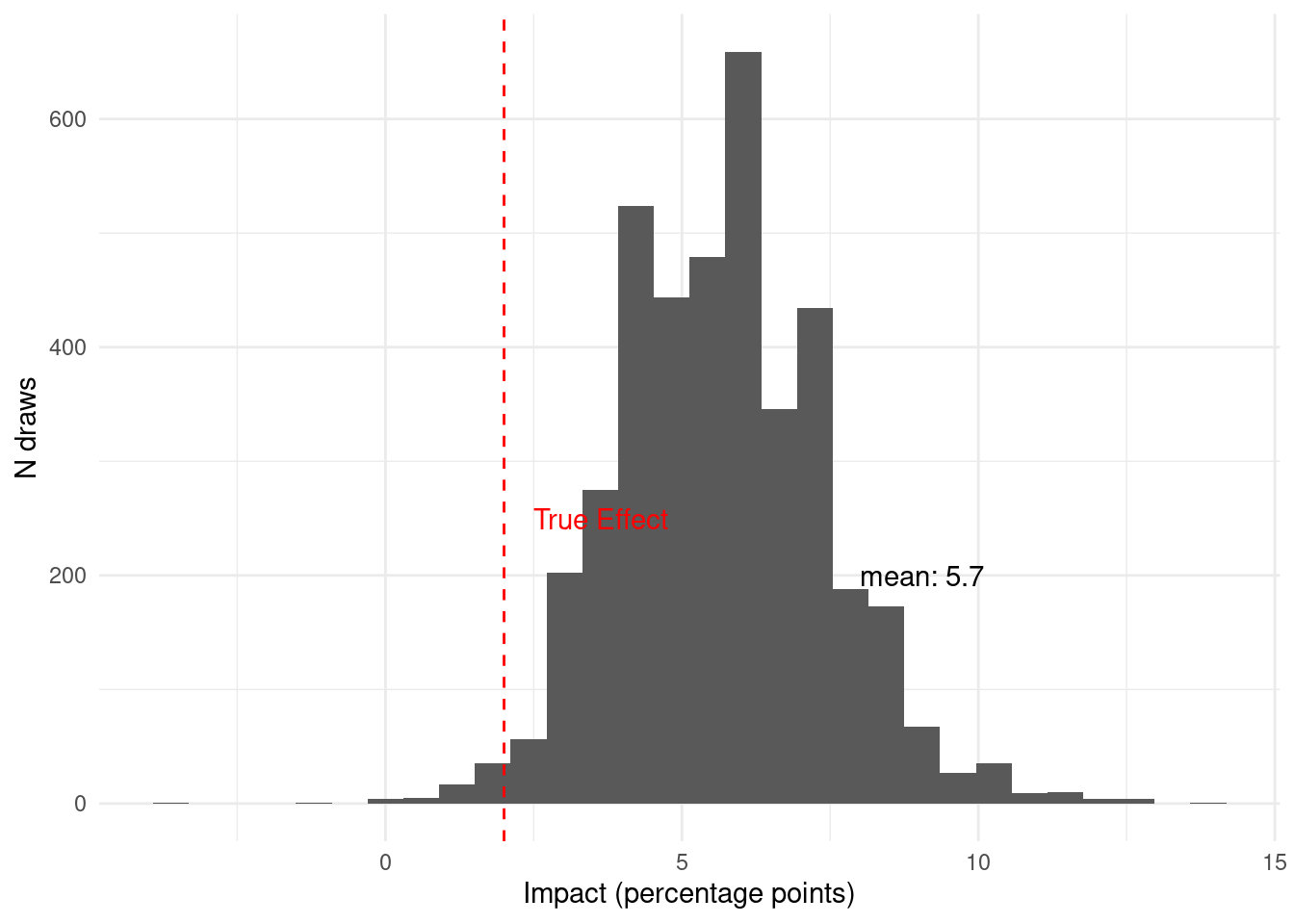

### Sequential Bayesian Updating with Incoming Data

Let's see how our model updates its beliefs as new data becomes available across

different time periods.

```{r}

#| warning: false

#| message: false

period_1 <- analyze_synthetic_data(

data = synthetic_data,

mean_alpha = -6,

sd_alpha = 1,

tau_mean = 2,

tau_sd = 2,

run_estimation = 1,

periods = c(1),

threshold = 0.01

)

# Print the plot

period_1$plot

```

Given the data available in period 1, we believe that the probability that the

intervention has a meaningful impact is

`r scales::percent(period_1$prob_above_threshold, accuracy = 0.1)`. This is with

just `r synthetic_data %>% filter(period == 1) %>% nrow()` observations. Now we

can see what happens as we see more data in period 2.

```{r}

#| echo: false

#| warning: false

#| message: false

period_1_2 <- analyze_synthetic_data(

data = synthetic_data,

mean_alpha = -6,

sd_alpha = 1,

tau_mean = 2,

tau_sd = 2,

run_estimation = 1,

periods = c(1,2),

threshold = 0.01

)

# Print the plot

period_1_2$plot

```

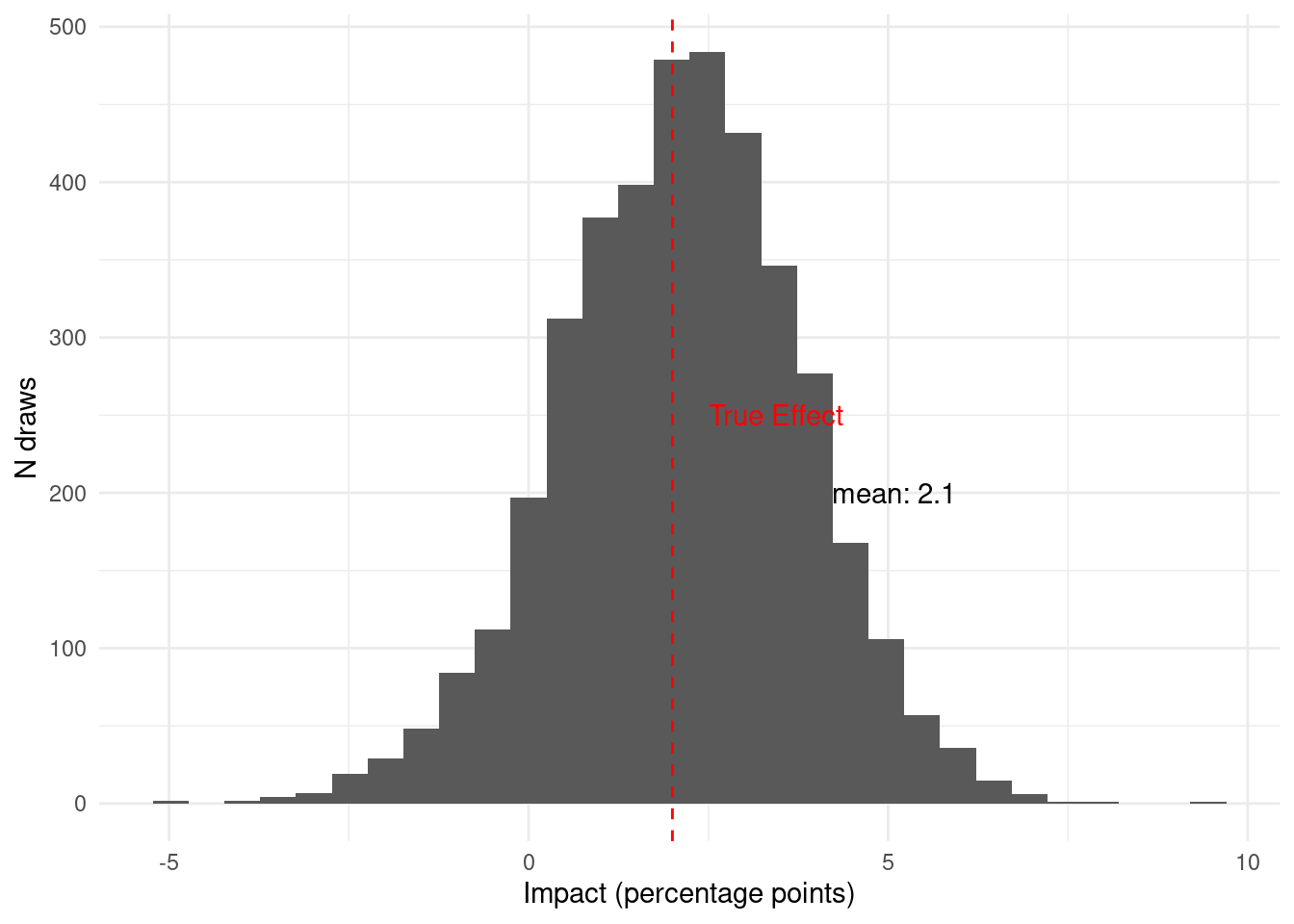

Now, given the data available in period 2, we believe that the probability that

the intervention has a meaningful impact is

`r scales::percent(period_1_2$prob_above_threshold, accuracy = 0.1)`. Notice

that new `r synthetic_data %>% filter(period == 2) %>% nrow()` observations from

period 2 move the posterior quite a bit. Finally, let's see how the data from

period 3 updates the posterior.

```{r}

#| echo: false

#| warning: false

#| message: false

period_1_2_3 <- analyze_synthetic_data(

data = synthetic_data,

mean_alpha = -6,

sd_alpha = 1,

tau_mean = 2,

tau_sd = 2,

run_estimation = 1,

periods = c(1,2,3),

threshold = 0.01

)

# Print the plot

period_1_2_3$plot

```

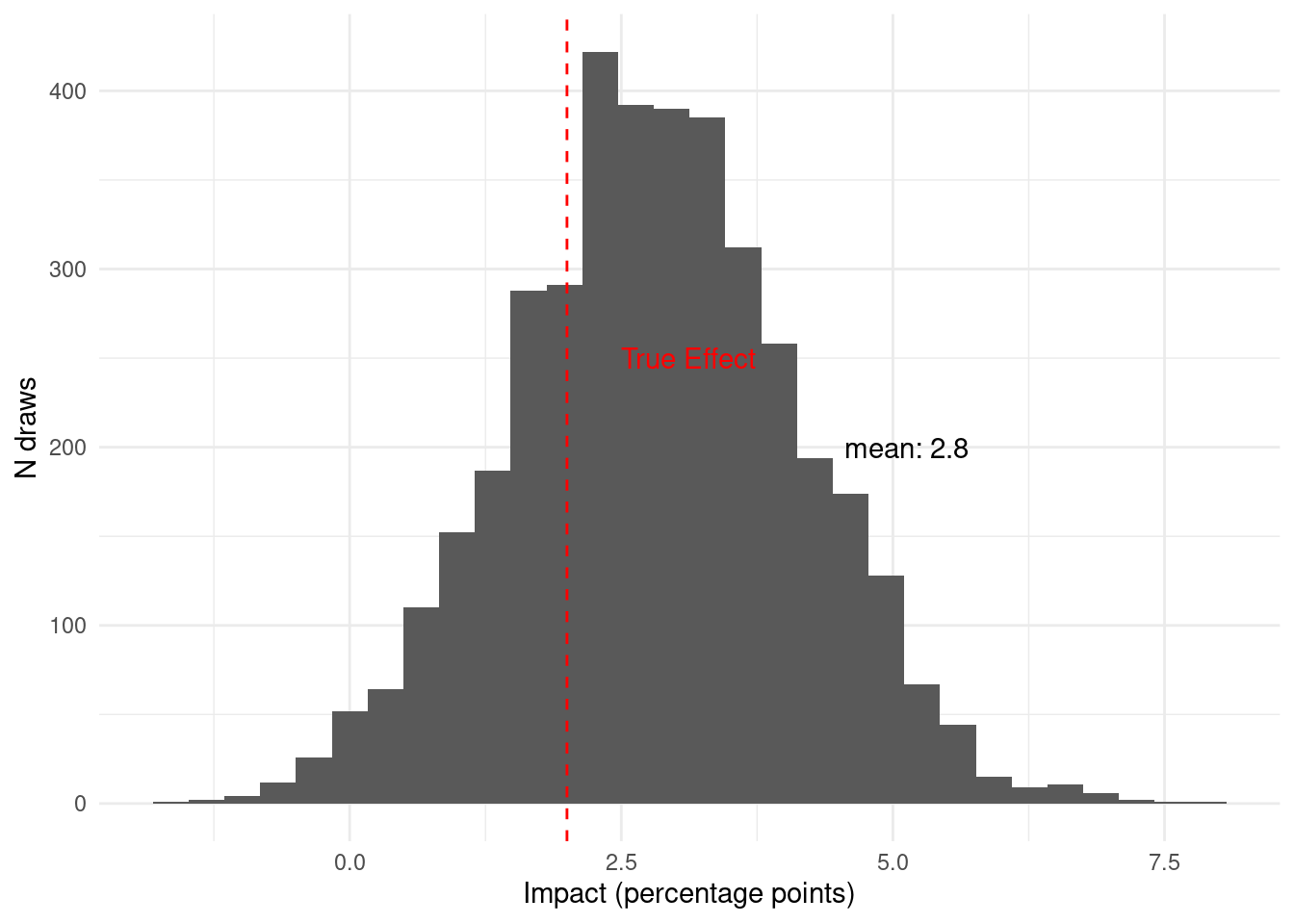

Once we have collected all the data from this pilot, Given the data available in

period 3, we believe that the probability that the intervention has a meaningful

impact is

`r scales::percent(period_1_2_3$prob_above_threshold, accuracy = 0.1)`.

One important thing to notice is that at any moment, including before collecting

any data, we could have made a decision. Then, as we collected more data our

belief changed.

### Calculating the Strength of a Pilot

To calculate the strength of a pilot, we can run a simulation like the one above

many times and see how often we would make the right decision. Moreover, we can

do this under different assumptions.

For all our simulations, we will use the following decision rule: if the

posterior probability that the impact exceeds 1 percentage point is greater

than 75%, we kill the new feature; otherwise, we launch it. For the first set of

simulations, we will assume that the true impact is an increase in churn of 2

percentage points; therefore, killing the new feature is the right choice. We

will also run these simulations assuming our pilot will have 2000 observations,

half in treatment and half in control.

```{r}

run_simulations <-

function(N,

num_observations,

treatment_proportion,

control_churn_prob,

treatment_churn_prob,

period1_proportion,

period2_proportion,

mean_alpha,

sd_alpha,

tau_mean,

tau_sd,

periods,

threshold,

num_cores = max(1, parallel::detectCores() - 1)) {

# Function to run a single simulation

run_single_sim <- function(i) {

# Generate synthetic data with a unique seed

synthetic_data <- generate_synthetic_data(

seed = i,

# Use simulation number as seed

num_observations = num_observations,

treatment_proportion = treatment_proportion,

control_churn_prob = control_churn_prob,

treatment_churn_prob = treatment_churn_prob,

period1_proportion = period1_proportion,

period2_proportion = period2_proportion

)

# Analyze the synthetic data

analysis_result <- analyze_synthetic_data(

data = synthetic_data,

mean_alpha = mean_alpha,

sd_alpha = sd_alpha,

tau_mean = tau_mean,

tau_sd = tau_sd,

run_estimation = 1,

# Run estimation

periods = periods,

threshold = threshold

)

return(analysis_result$prob_above_threshold)

}

# Run simulations using purrr (parallel or sequential)

probabilities <- 1:N %>%

{

if (num_cores > 1) {

# Use future_map_dbl for parallel execution

future::plan(future::multisession, workers = num_cores) # Setup parallel processing

furrr::future_map_dbl(., run_single_sim, .options = furrr::furrr_options(seed = TRUE, packages = "rstan"))

} else {

# Use map_dbl for sequential execution

purrr::map_dbl(., run_single_sim)

}

}

return(probabilities)

}

```

Let's run the simulations with 2000 observations:

```{r}

#| warning: false

#| message: false

#| cache: true

simulations <- run_simulations(

N = 200,

num_observations = 2000,

treatment_proportion = 0.5,

control_churn_prob = 0.05,

treatment_churn_prob = 0.07,

period1_proportion = 0.2,

period2_proportion = 0.5,

mean_alpha = -6,

sd_alpha = 1,

tau_mean = 2,

tau_sd = 2,

periods = c(1, 2, 3),

threshold = 0.01,

num_cores = max(1, parallel::detectCores() - 1)

)

```

The simulation results tell us that, with our chosen priors, model, pilot size,

and decision rule, we correctly kill the new feature (when it truly has a

meaningful impact) in approximately

`r scales::percent(mean(simulations > 0.75))` of the simulated pilot studies.

Next we can run this simulation under the assumption that instead of 2000

observations we will only have 1000 observations.

```{r}

#| warning: false

#| message: false

#| cache: true

simulations <- run_simulations(

N = 200,

num_observations = 1000,

treatment_proportion = 0.5,

control_churn_prob = 0.05,

treatment_churn_prob = 0.07,

period1_proportion = 0.2,

period2_proportion = 0.5,

mean_alpha = -6,

sd_alpha = 1,

tau_mean = 2,

tau_sd = 2,

periods = c(1, 2, 3),

threshold = 0.01,

num_cores = max(1, parallel::detectCores() - 1)

)

```

Now we can see that if the pilot only has 1000 observations, we would make the

right decision only `r scales::percent(mean(simulations > 0.75))` of the time.

Similarly, we can now change our data generating process so that the true effect

of the intervention is zero. In the right decision would be to roll out the new

feature.

```{r}

#| warning: false

#| message: false

#| cache: true

simulations <- run_simulations(

N = 200,

num_observations = 1000,

treatment_proportion = 0.5,

control_churn_prob = 0.05,

treatment_churn_prob = 0.05, # <-same as control_churn_prob

period1_proportion = 0.2,

period2_proportion = 0.5,

mean_alpha = -6,

sd_alpha = 1,

tau_mean = 2,

tau_sd = 2,

periods = c(1, 2, 3),

threshold = 0.01,

num_cores = max(1, parallel::detectCores() - 1)

)

```

In this case, the probability of making the right choice (rolling out the new feature when it has no meaningful impact on churn) is `r scales::percent(mean(simulations < 0.75))`.

::: callout-tip

## Learn more

- @dong2013powerup PowerUp!: A tool for calculating minimum detectable effect sizes and minimum required sample sizes for experimental and quasi-experimental design studies.

- @bloom2008core The core analytics of randomized experiments for social research.

- @gelman2014beyond Beyond power calculations: Assessing type S (sign) and type M (magnitude) errors.

- @mcdonnell2018test Test & Roll: Profit-Maximizing A/B Tests.\

:::